You’ve found the perfect place in California. Maybe it’s a cozy apartment in Santa Monica, or a spacious house in the Inland Empire. You’ve signed the lease, bought new furniture, and then… you remember insurance. Specifically, renters insurance. It’s often an afterthought, sometimes even a landlord requirement, but it’s never just a box to check. It’s a shield for your stuff and your financial well-being.

Here’s what you’ll learn in this guide:

- Why renters insurance isn’t optional for most Californians.

- The core differences in coverage when you rent an apartment versus a house.

- How to figure out exactly how much protection you need.

- What makes your premium go up or down, especially in California.

- Practical steps to get the right policy for your situation.

Understanding Renters Insurance: More Than Just Your Landlord’s Request

Most people think renters insurance just covers their belongings if there’s a fire or a break-in. That’s part of it, sure. But it’s far from the whole story. Imagine your apartment building’s sprinkler system malfunctions, flooding your unit and the one below. Or a guest slips on your patio at your rented house, breaking an arm. These aren’t just inconveniences; they’re potentially ruinous financial disasters.

Renters insurance typically breaks down into three main categories:

- Personal Property Coverage: This protects your stuff – furniture, electronics, clothes, jewelry – from covered perils like fire, theft, vandalism, and certain weather events. It’s not just while it’s in your home, either. Often, it covers items stolen from your car or even while you’re on vacation.

- Liability Coverage: This is a big one. If someone is injured in your rented space, or if you accidentally cause damage to the property of others (like that sprinkler example), your liability coverage can help pay for medical bills, legal fees, and repair costs. This is where the real peace of mind comes in.

- Loss of Use (Additional Living Expenses): What if a fire makes your place unlivable for a few weeks or months? This part of your policy helps cover temporary housing costs – like a hotel room or another rental – and even extra food expenses while your home is being repaired.

You’re probably starting to see why it’s not just a nice-to-have. It’s pretty essential, no matter what kind of home you’re renting.

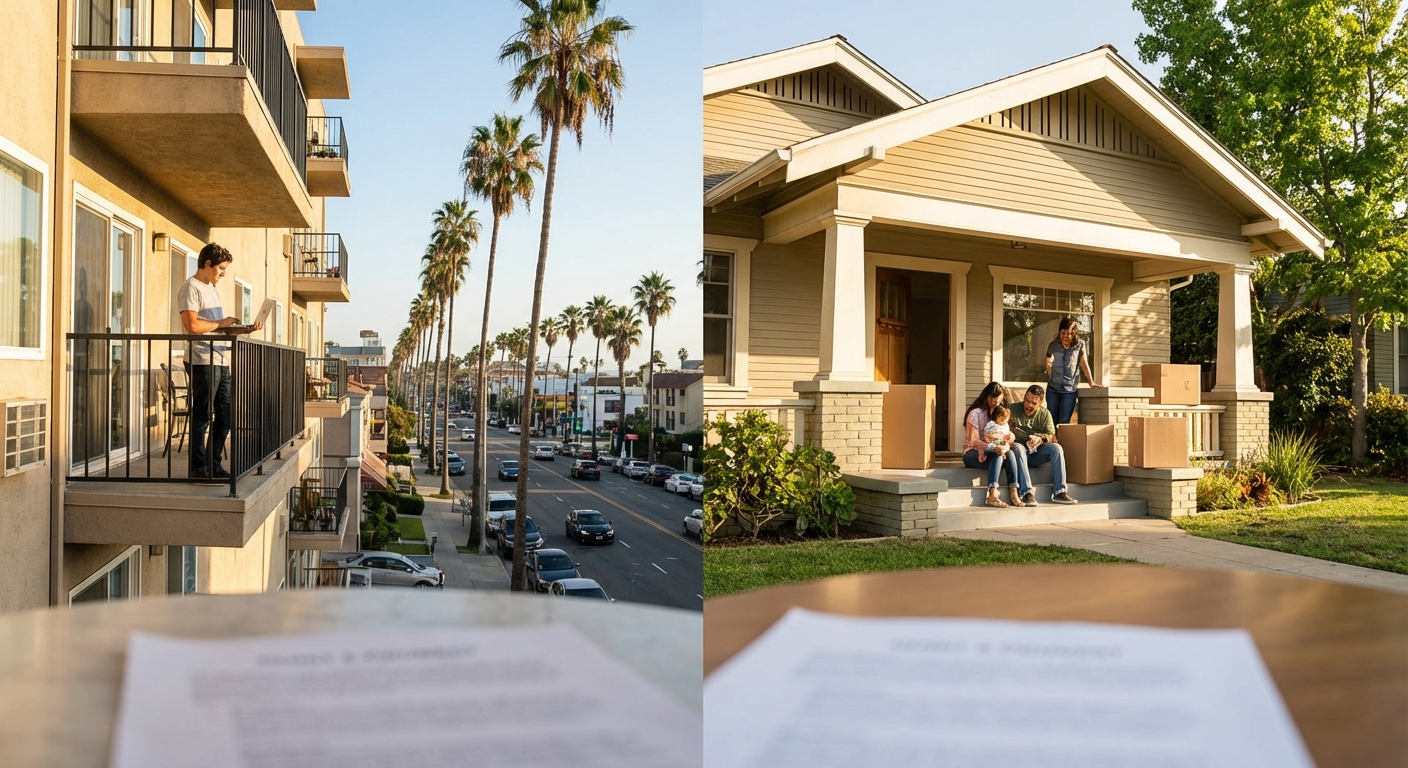

Apartment vs. House: What Changes for Renters Insurance?

The core coverage types stay the same whether you’re in a high-rise in downtown San Diego or a suburban home in Sacramento. But the *amount* of coverage you need, and even some of the risks, can shift quite a bit. It’s not always obvious.

The Personal Property Question

Think about how much stuff you own. Most people underestimate this dramatically. A quick walk through your apartment or house – really looking at everything from your kitchen gadgets to your wardrobe – will open your eyes. Often, renters in houses tend to have more outdoor gear, tools, or larger furniture pieces simply because they have more space. They might also have more sentimental items accumulated over years.

But here’s the thing. An apartment dweller might have equally valuable possessions crammed into a smaller space. High-end electronics, designer clothes, valuable art – these aren’t exclusive to house renters. The key is taking a detailed inventory, regardless of your dwelling type. Don’t forget those bikes in the garage or the expensive camera gear you use for weekend trips to Yosemite.

Liability: Shared Walls vs. Private Yards

This is where the apartment vs. house distinction can get interesting. In an apartment, you’re sharing walls, floors, and ceilings with neighbors. A plumbing leak in your unit could easily damage the apartment below. A fire could spread faster. Your liability risk might involve shared common areas, too, if you’re responsible for a guest’s injury there.

For house renters, the liability picture often changes to include a yard. Maybe a dog bite incident. Perhaps a guest trips on uneven paving stones. You might have a trampoline or a pool, which are huge liability magnets. Even if you don’t own the property, you’re still responsible for maintaining a safe environment for visitors. A house often comes with more opportunities for things to go wrong on the property itself, simply because there’s more of it.

Loss of Use: Displacement Scenarios

If a disaster strikes, both apartment and house renters face displacement. But the logistics can differ. If your apartment building has a major fire, it might be months before repairs are done, and finding comparable temporary housing in a tight California market can be tough. A house might offer more flexibility in terms of repair timelines, but the impact of being out of your home is the same.

Your policy should cover reasonable additional living expenses, but what’s “reasonable” can vary. Make sure you understand your limits here. Living in a hotel for weeks in Ventura County or the Valley isn’t cheap.

Step-by-Step: Getting the Right Coverage

Okay, so you know what renters insurance does. Now, how do you actually get the policy that fits *your* life?

1. Inventory Your Belongings – Seriously

This is the most tedious, yet most important, step. Go room by room. Take photos or videos. List everything. For expensive items, keep receipts or appraisals. Use a spreadsheet. It sounds like a chore, and it is, but it’s invaluable if you ever need to file a claim. Without it, proving what you owned and its value becomes a nightmare. Consider whether you want replacement cost value (RCV), which pays for a brand-new item, or actual cash value (ACV), which factors in depreciation. RCV costs a bit more but is almost always worth it.

2. Assess Your Liability Exposure

Think about your lifestyle. Do you entertain often? Do you have pets? Is your rented house on a busy street? Do you have a lot of outdoor equipment that could cause an accident? If you have a dog, especially certain breeds, some insurers might charge more or even deny coverage. Be honest about your risks. You might want to consider higher liability limits than the minimum, especially in a litigious state like California. A common minimum is $100,000, but $300,000 or even $500,000 provides much better protection for only a small bump in premium.

3. Understand California’s Unique Risks

California isn’t just sunshine and beaches. We have earthquakes, wildfires, and sometimes, even mudslides in areas like the Santa Cruz Mountains or parts of Malibu. Standard renters insurance doesn’t cover earthquakes or floods. You’ll need separate endorsements or policies for those. If you’re renting a house in a brush fire zone – say, near the hills of Los Angeles or parts of Sonoma County – your premiums might reflect that risk, and some insurers might even be hesitant to offer coverage without specific wildfire mitigation efforts by the landlord.

The insurance market in California has been turbulent. Property insurance premiums across the state have seen some wild swings lately. Some folks in brush fire zones have seen their homeowner’s rates jump 40% or more between 2022 and 2024, and while renters insurance isn’t quite that volatile, it’s still affected by the overall market. Carriers like State Farm, AAA, and Farmers are all adjusting to new realities, including the state’s FAIR Plan changes and the ongoing discussions around Prop 103.

4. Get Multiple Quotes and Compare

Don’t just go with the first quote you get. Different insurers have different appetites for risk and different pricing models. This is where an independent insurance agent becomes invaluable. They work with multiple carriers and can shop around for you.

Finding the right policy can feel like a maze. That’s where an independent agent like Karl Susman from California Renters Protection, CA License #OB75129, really helps. They know the California market inside and out and can help you compare options from various companies. You can start by getting a quote right now at californiarentersprotection.com/quote/.

5. Review Your Policy Annually

Life changes. You buy new things. You get a new pet. Your landlord makes improvements. Your policy needs to keep up. Take five minutes each year to review your coverage limits and make sure they still align with your current situation. It’s a simple step that can save you a lot of headaches later.

Common Renters Insurance Questions in California

Q: Does my landlord’s insurance cover my belongings?

A: Absolutely not. Your landlord’s insurance covers the building itself – the structure. It doesn’t cover your personal property or your personal liability. That’s why renters insurance is so important for you.

Q: Is renters insurance expensive in California?

A: Not usually! Compared to homeowner’s insurance, renters insurance is quite affordable. Many policies in California cost less than $20 a month. Of course, this varies based on your location, coverage amounts, and deductible. But for the peace of mind it offers, it’s a bargain.

Q: Do I need earthquake insurance?

A: Standard renters insurance doesn’t cover earthquake damage. Given California’s seismic activity, it’s something to seriously consider. You can often add an earthquake endorsement to your renters policy or purchase a separate policy through the California Earthquake Authority (CEA). It’s an extra cost, but if you live in an active fault zone, it’s well worth exploring.

Q: What if I have a roommate?

A: This gets tricky. Some policies might cover all residents listed on the lease, but many don’t. It’s best for each roommate to have their own policy to ensure adequate personal property and liability coverage. Don’t assume you’re covered by your roommate’s policy.

Q: Can I save money on my premium?

A: Often, yes. Many insurers offer discounts for things like having smoke detectors, deadbolt locks, or a home security system. Bundling your renters insurance with your auto insurance is another common way to save a few bucks. Always ask about available discounts.

So, whether you’re settling into a new apartment or a rented house, knowing you’re protected lets you focus on what really matters: enjoying your California life. To get started, reach out to an expert like Karl Susman at California Renters Protection, CA License #OB75129, or visit californiarentersprotection.com/quote/ for a quick quote.

This article is for informational purposes only and does not constitute financial advice.