What You’ll Learn

- The essential difference between what renters insurance *does* and *doesn’t* cover for water damage.

- Why “sudden and accidental” is the magic phrase for most water-related claims.

- How flood, sewer backup, and tenant negligence fit into the picture.

- The critical role of personal property and liability coverage when water strikes.

- Why getting expert advice from a California-licensed agent like Karl Susman is a smart move.

The Unexpected Deluge: Why California Renters Need to Understand Water Damage Coverage

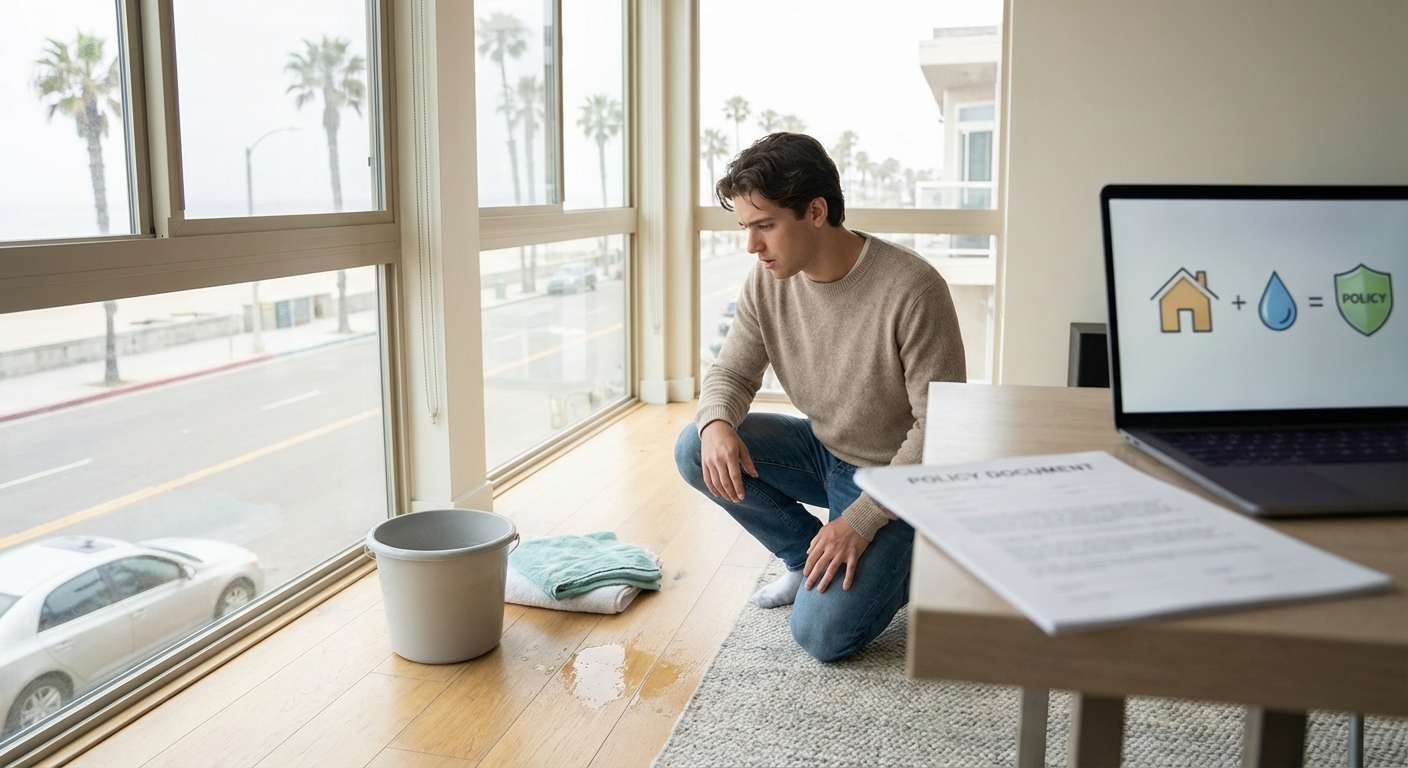

Imagine this: you’re in your cozy apartment in the Inland Empire. You wake up one morning, step out of bed, and splash. A pipe burst in the wall overnight. Water’s everywhere. Your new rug? Soaked. Your laptop on the floor? Fried. Your favorite sneakers? Floating. It’s a nightmare scenario, and it happens more often than you’d think, especially with California’s aging infrastructure and the recent swings between drought and atmospheric rivers.

So, you’ve got renters insurance, right? Good. But does it cover *this*? The short answer is yes. The real answer is more complicated.

Step 1: Your Renters Policy and the Watery Unknown

Renters insurance isn’t just about protecting your stuff from fire or theft. It’s a shield against many unexpected events, and water damage often sits right at the top of the list for California residents. Your policy generally has a few main parts: personal property coverage, liability coverage, and additional living expenses. Each plays a role when water wreaks havoc.

But here’s the thing. Not all water is created equal in the eyes of an insurance company.

Step 2: The Good News – What Water Damage *Is* Covered

Most standard renters insurance policies *do* cover water damage to your personal belongings if it’s sudden and accidental. This is the key phrase you need to remember.

Think about it:

- A burst pipe in your kitchen wall.

- An overflowing bathtub because your toddler turned the faucet on and left it.

- A leaky washing machine hose that floods your laundry nook.

- Rain coming in through a hole in the roof or a broken window, if that hole or break was sudden and unexpected (like from a falling tree branch).

- A fire sprinkler system accidentally discharging.

In these scenarios, your policy would typically help pay to repair or replace your damaged personal property – your furniture, clothes, electronics, and other items. It’s designed to put you back in the position you were in before the mishap.

Step 3: The Not-So-Good News – What Water Damage *Isn’t* Covered (Usually)

This is where many people get tripped up. While sudden and accidental water damage is covered, a few big exceptions exist.

Flood Damage

This is the biggest one. Standard renters insurance policies, whether from State Farm, AAA, or Farmers, *do not* cover damage caused by natural flooding. That means if the Santa Ana River overflows its banks after a heavy storm and floods your ground-floor apartment in Orange County, your renters policy won’t cover your soaked possessions. For that, you’d need a separate flood insurance policy, usually through the National Flood Insurance Program (NFIP).

Sewer and Drain Backup

Imagine your toilet backs up, or the main sewer line clogs and sewage bubbles into your apartment. Gross, right? Standard policies often exclude this. However, you can usually add an endorsement – a rider – to your renters policy to cover sewer and drain backup. It’s a smart addition, especially in older buildings or areas with known infrastructure issues.

Gradual Damage and Neglect

Remember “sudden and accidental”? The opposite of that is gradual damage. If a leaky faucet drips for six months, slowly rotting the cabinet underneath, your policy probably won’t cover it. Why? Because it’s considered a maintenance issue, something you should have fixed. Insurance is for unexpected events, not for things that could have been prevented with regular upkeep. If you leave a window open during a storm and your apartment gets soaked, that’s often considered neglect, and your claim could be denied.

Step 4: Your Stuff vs. The Landlord’s Stuff

When water damage hits, it’s easy to get confused about who pays for what. Let’s make it clear:

- Your Renters Insurance: Covers *your* personal property (furniture, clothes, electronics, etc.) and your liability if you accidentally cause damage to the building or another tenant’s property.

- Your Landlord’s Insurance: Covers the *structure* of the building itself – the walls, floors, fixtures, and appliances that came with the unit. It also covers their personal property, if any.

So, if a pipe bursts in your wall, your landlord’s policy would pay to fix the wall and the pipe. Your renters insurance would pay to replace your ruined sofa and laptop. Big difference.

Step 5: When You Can’t Go Home Again – Additional Living Expenses

Sometimes, water damage is so severe you can’t live in your apartment while repairs are being made. Maybe the entire kitchen needs to be ripped out, or there’s a serious mold problem. This is where the “additional living expenses” (ALE) portion of your renters policy kicks in.

ALE coverage helps pay for temporary housing – a hotel, or even a short-term rental – and other necessary costs like extra food expenses (because you can’t cook at home) or laundry services. It’s designed to cover the *increase* in your living costs while your home is uninhabitable. It won’t pay for a luxury suite if you were living in a studio, but it’ll keep you comfortable until you can move back in.

Step 6: The “Oops, My Fault” Factor – Liability Coverage

What if the overflowing bathtub wasn’t just *your* problem, but also caused water to leak through the ceiling into the apartment below? Now your neighbor’s new flat-screen TV is ruined. This is precisely why liability coverage is so important.

Your renters insurance liability portion would step in to cover the costs of repairing your neighbor’s property or even their medical bills if they slipped and fell on the water you caused. It also covers legal defense costs if they decide to sue you. Most policies offer coverage starting at $100,000, but many renters opt for higher limits – like $300,000 or even $500,000 – for extra peace of mind. A small increase in your premium can mean a huge difference if you face a significant claim.

Step 7: California’s Unique Water Challenges

Living in California means living with extremes. We see scorching dry spells, then sudden, intense atmospheric rivers that dump inches of rain in hours. Think back to the storms that hammered Ventura County and the Valley last winter, causing widespread flooding and mudslides. Older buildings, common in cities like Los Angeles and San Francisco, often have plumbing systems that are decades old and more prone to bursting. Coastal areas, like those in San Diego or along the Central Coast, face different risks from storm surges.

Understanding these local risks can help you gauge your own vulnerability to water damage and ensure your coverage is adequate.

Step 8: Reading Your Policy – It’s Not Just Paperwork

Honestly, most people just file their insurance policy away without ever truly reading it. But if you want to understand your water damage coverage, you need to crack it open. Look for the “Perils Covered” section to see what events your personal property is protected against. Then, find the “Exclusions” section – this is where you’ll see what’s *not* covered, like flood or gradual water damage.

Don’t be afraid to ask questions. That’s what a good agent is for.

Step 9: Getting the Right Coverage for Your California Rental

Choosing the right renters insurance isn’t a “set it and forget it” task. Your needs change, and so do the risks. Maybe you’ve bought more expensive electronics, or you’ve moved to a ground-floor apartment in an area prone to heavy rains.

This is exactly where a knowledgeable local expert comes in. Karl Susman of California Renters Protection, CA License #OB75129, has been helping California renters protect their homes and belongings for years. He understands the nuances of water damage coverage in our state, from the specific risks in the Bay Area to the challenges in the desert communities. A quick conversation can clarify exactly what you need.

Want to see what protecting your California rental could look like? Get a personalized renters insurance quote today: https://californiarentersprotection.com/quote/

You can always reach Karl and his team at (877) 411-5200 for advice tailored to your situation.

Frequently Asked Questions About Renters Insurance and Water Damage

Is flood insurance included in standard renters policies in CA?

No, it’s not. Standard renters insurance policies in California (or anywhere else, for that matter) specifically exclude damage from natural flooding. If you live in a flood-prone area, you’d need to buy a separate flood insurance policy, usually through the National Flood Insurance Program (NFIP).

What if my landlord’s pipe bursts and damages my stuff?

Your renters insurance would cover your personal property damage in this scenario. Your landlord’s insurance would cover the damage to the building itself. If the landlord’s negligence caused the pipe to burst (e.g., they ignored obvious maintenance issues), your renters policy might subrogate against their policy to recover your deductible.

Does renters insurance cover mold?

This is a tricky one. Most standard renters policies don’t cover mold unless it’s a direct result of a covered peril, like a sudden burst pipe. Even then, coverage might be limited. If the mold developed gradually due to humidity or an unrepaired slow leak, it’s generally not covered. Some insurers offer mold remediation endorsements, but they’re not standard.

How much water damage coverage do I really need?

It depends on the value of your personal belongings. Most people underestimate how much their stuff is worth. Create a home inventory. For liability, consider at least $100,000, but many renters opt for $300,000 or more, especially if they live in an apartment building where their actions could affect neighbors. For additional living expenses, make sure it’s enough to cover temporary housing for several weeks or months.

What’s the difference between “sudden and accidental” and “gradual” water damage?

“Sudden and accidental” means the water damage happened unexpectedly and quickly – a pipe burst, a washing machine hose snapped, a storm blew a window out. “Gradual” means the damage occurred slowly over time, like a persistent leaky faucet that wasn’t fixed, or condensation causing rot. Renters insurance generally covers sudden and accidental events, not gradual ones, as gradual damage is often considered a maintenance issue.

Ready to secure your peace of mind? Don’t wait until the water starts flowing. Get your personalized renters insurance quote here: https://californiarentersprotection.com/quote/

***

This article is for informational purposes only and does not constitute financial advice.